Widespread concessions are weakening effective rents and contributing to distress in the multifamily market, particularly in areas still absorbing recent high levels of apartment construction, new research from investment management firm Colliers shows. At the same time, multifamily REIT executives widely reported decreases in free-rent incentives in their first-quarter reports. So what’s going on?

This a situation where the overall numbers don’t tell the whole story, according to LeaseLock Chief Economist Greg Willett.

Although REITs recently cited declining rent concessions, “key industry data providers like CoStar, RealPage, Inc. and Yardi Matrix all report that concession usage is broadening so far in 2026 and that the size of the typical discount is still substantial,” Willett said in a LinkedIn post.

“Both of these perspectives can be true, and that actually is the case seen when digging into the data details.”

Concession dollars were at a record high in the first quarter — averaging $129 per unit — but only about a quarter of units offered incentives, signaling that discounts are concentrated in certain asset types and geographies, according to Colliers.

“Only 25.4% of units are offering concessions today, far below the 64.2% peak seen in late 2009, indicating incentives are concentrated in supply-pressured pockets rather than broadly distributed across the market,” per Colliers.

Discounts persist

Zillow also reported high discount rates in its May 27 report: Nearly 40% of rentals on its platform offered concessions this spring, a 5-percentage-point increase from a year ago. Its share of listings with concessions has more than doubled since before the pandemic.

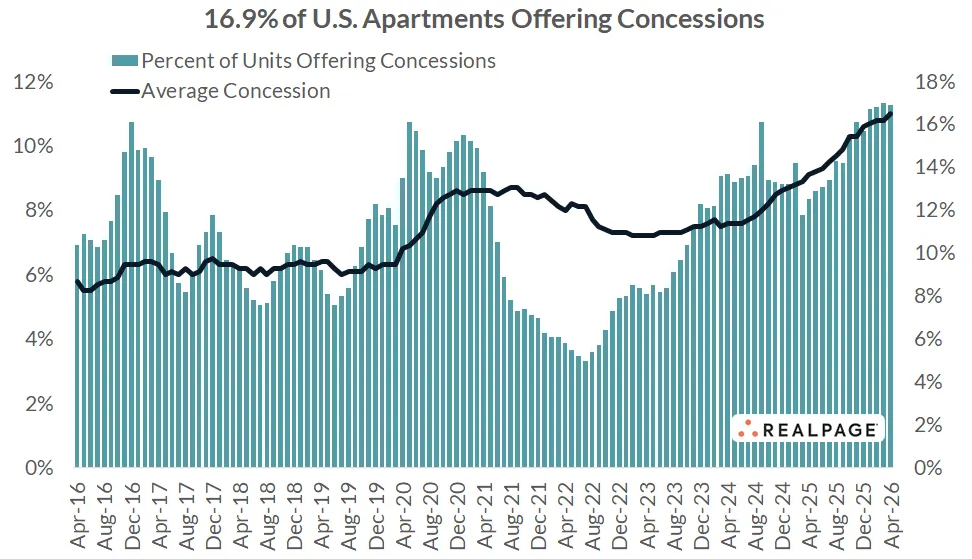

In April, RealPage reported average national concession use at 16.9% among stabilized apartments, a 4.4-point year-over-year uptick and near the highest monthly level since mid-2014, according to its May 27 report. The average discount was 11% in April, up 1.9 points YOY, which works out to nearly six weeks free on a 12‑month lease.

Concessions have generally trended up since mid-2016 and remain at the highest level since the post-financial-crisis period in 2010, per RealPage.

Now, despite otherwise steady metrics, underlying stress in multifamily housing is becoming more visible as operators offer discounts to prioritize occupancy, according to Colliers. Some assets that were underwritten to aggressive post-pandemic rent expectations are straining under the lower-than-anticipated cash flow.

“Concessions have become a structural feature of the current leasing environment, though the pattern differs from the [global financial crisis],” per Colliers. “Multifamily stress is emerging selectively, driven less by occupancy erosion and more by the combined effects of elevated concessions, muted effective rent growth, and refinancing pressure.”

In proportional terms, though, the “concession burden” is less severe than during the global financial crisis period, according to Colliers. “Concessions represent 7.2% of asking rent in Q1 2026 versus 9.2% at the GFC peak, reinforcing that today’s concession environment is elevated but not as universally disruptive.”

Tyler Chesser, co-founder and managing partner of CF Capital, previously told Multifamily Dive that the wall of multifamily maturities hitting this year will be a big driver of transaction volume. Some investors expect more problem properties to hit the market, whether offered by owners or banks, and ignite the sales market.

Economist Jay Lybik, senior director of market research at Continental Properties, said there appear to be active buyers for those properties, so true distress doesn’t seem to be an issue right now.

“What I have heard is that many developers that have projects in trouble are just selling them and either breaking even or taking a loss as opposed to having a project go back to the lender,” Lybik told Multifamily Dive in an email.

Class matters

Concession use diverges greatly by product class, with discounts elevated among older apartments but waning in the luxury segment. RealPage’s data shows that class C units continued to see markedly higher discounts, averaging 23.4% in April, than class A and class B apartments, at 13.2% and 14.5%, respectively.

“REIT asset holdings generally consist of better-quality properties that command substantial rents and face competition from new supply coming into the market. Available pricing stats show that discounts in this product space are beginning to retreat at least a little, now that delivery volumes are moving past peak,” Willett said.

On the other hand, concession usage in middle-market class B communities has been mixed in the key industry data sets, headed up in some locations but down in others, according to Willett.

“The real movement is in the bottom-tier Class C properties. Stats for that segment of the market show the share of product offered with price discounts skyrocketing over the course of the past year,” Willett said.

The Trump administration’s immigration crackdown is one factor affecting class C housing, particularly in states like Florida and Texas, where managers reported that they have seen occupancy fall in the wake of U.S. Immigration and Customs Enforcement raids.

“The loss of immigrant households has drastically reduced the number of prospects for the lowest-priced product in locations where international newcomers form an especially important component of the renter base,” according to Willett.

Regional variation

A wave of apartment construction, particularly across the Sun Belt, has pushed the national rental vacancy rate to 7.3% this year — up from just 5.6% in 2021, according to Zillow. Amid such pressure, concessions are up from year-ago levels in 44 of the 50 largest metro areas.

Although multifamily REITs cited tapering concessions, the majority of their footprints are outside of the hardest-hit markets, according to Lybik.

For example, “a recent analysis of the Phoenix multifamily market showed that over the past six months, the number of properties built since 2023 that are offering 10 weeks free has skyrocketed. Currently, properties containing just over 30,000 units are offering 10 weeks free,” Lybik said, citing internal data.

“Concessions are a tool, but operators who pair them with the best renter experience complete with fast responses, clear terms and easy move-in will see better retention when the market tightens again.”

Kara Ng

Senior economist at Zillow

The operators feeling the most pressure are in Sun Belt metros where apartment construction has boomed, Kara Ng, senior economist at Zillow, told Multifamily Dive in an email. “Those operators are competing hardest for a smaller pool of renters relative to the available supply.”

The markets with the highest share of concessions are Denver (68.3%), Charlotte, North Carolina (66.6%), Dallas (64.2%), Austin, Texas (63.8%), and Nashville (62.6%), per Zillow.

By contrast, incentives are lowest in areas where competition among renters remains fierce: Buffalo, New York (11.1%), Providence, Rhode Island (12.6%), New York City (18.4%), New Orleans (19.2%), and Chicago (21.7%).

Looking ahead

The high levels of supply driving these concessions didn't appear overnight and won't unwind quickly, according to Ng. The pipeline of new units still being absorbed means operators in high-construction markets will likely face pressure well into 2027.

“Concession levels may plateau or tick down slightly as new supply is absorbed, but a quick reversal to pre-pandemic norms is unlikely,” Ng said. “Multifamily pros should plan for a market where renters have leverage and price concessions are a cost of doing business, not an exception.”

Overall, apartment starts have slowed meaningfully, laying the groundwork for higher rents next year, “particularly in markets further along the absorption curve,” per Colliers.

For now, though, concessions persist, according to Lybik.

“I think the industry will continue to see heavy use of concessions for the rest of 2026 because consumers have become too accustomed to them and operators will fear trying to be the first mover to pull back the use,” Lybik said. “It’s the age-old economic prisoner’s dilemma.”

This is an important moment for operators to rethink how they communicate value, according to Ng. Renters aren't just looking for the lowest rent — they're also evaluating upfront costs, lease flexibility and what it's actually like to live in a place. Operators who list concessions prominently, offer flexible tour options and remove friction from the application process will have an edge.

“Concessions are a tool, but operators who pair them with the best renter experience complete with fast responses, clear terms and easy move-in will see better retention when the market tightens again,” Ng said.

“The data tells us renters have more options than they've had in decades. The operators who treat them accordingly will be better positioned when supply and demand rebalance.”

Click here to sign up to receive multifamily and apartment news like this article in your inbox every weekday.